When will we get serious about nuclear? (or something 'nuclear-esque'?)

The ten biggest questions in energy & climate tech, Question 2

Current hypothesis: the 2030s

The big question for nuclear is almost certainly “when”, not “if”.

I wish it weren’t so, but I’ve grown increasingly confident that bottlenecks on electric transmission development and other constraints on siting wind & solar projects are likely to become major limiting factors on the growth of renewables. (See Question 1…) I believe these limitations will grow increasingly apparent through the 2020s, and will be undeniable by the early 2030s. By then, the world will realize that complete global decarbonization will require another globally-scalable, zero-carbon primary energy resource. Ideally, this resource ought to provide firm, reliable, 24/7 energy supply; even more crucially, it must be extremely power dense.1 We need to be able to plop it down easily in & around large population centers. What we’re looking for is basically a one-for-one replacement for all of our coal-fired power plants… just without the emissions.

Of course, you know I’m teasing: we already have this magical resource. We have for a long time. In fact, we built the first nuclear plants before the invention of the computerized spreadsheet, and most of those plants are still operating at 90% capacity factors today.2 I repeat: we currently rely on a fleet of nuclear power plants for which key operational and safety calculations were done by hand. By people who thought margarine was the future! And this fleet is arguably the safest source of energy, per joule of energy produced, by nearly any reasonable definition of “safe”. Apart from Chernobyl, there are zero deaths directly attributable to nuclear power plants, globally.3

So, deploying nuclear power is not fundamentally a technology problem. It’s a public opinion and regulatory problem.

The US pioneered nuclear power, and we were mid-way through a construction boom when a reactor on Three Mile Island partially melted down, in 1979. The national response to that incident caused costs to balloon and timelines to stretch for plants already under construction - in some cases for decades. We then basically gave up trying to build new nuclear plants at all for the next twenty years. To this day, public opinion polls continue to register strong disapproval of nuclear energy, especially when it’s located In My Backyard. Even nuclear’s friends among the public don’t want to live within 100 miles of a nuclear plant.

This public relations problem underpins nuclear’s regulatory problem. Where the public has turned against nuclear, governments have turned against nuclear…and it’s nearly impossible to sustain a nuclear program without a supportive policy & regulatory framework - or at least a neutral one. In the US, we have the Nuclear Regulatory Commission, or NRC, whose offical job is to oversee nuclear safety & security, but whose putative job appears to be making it impossible to cost-effectively build new nuclear plants. The NRC also seems intent on making it impossible to affordably license new reactor designs.

NRC regulations are notoriously inflexible, and its processes are almost a parody of bureaucratic excess. In the words of one of my nuclear expert friends (who shall remain nameless): “You need NRC approval to move a porta-potty on a nuclear construction site.” Meanwhile NuScale, the only ‘next-generation’ reactor design to be approved by the NRC to date, reportedly spent $500m alone in pursuit of its license. To be clear: this money wasn’t spent on R&D or prototype development; it was spent on consultants and lawyers that NuScale needed in order to progress through the licensing process!

Back in 1999, the staff of the NRC wrote a white paper on the need for more “risk-informed, performance-based” regulation. In other words, more than twenty years ago, the NRC recognized the need for more speed & agility to approve projects whose safety could be validated - even if those projects deviated from established designs or processes. Twenty years later, with no visible progress towards this goal, Congress passed the bipartisan “Nuclear Energy Innovation & Modernization Act” which told the NRC that it was required to develop & implement exactly this kind of more flexible regulation. However, the deadline Congress set is December 2027, and the commission’s first draft of the plan is not inspiring confidence.

In the meantime, as over two decades have passed, the first new nuclear plant built in the US in ages was conceived, developed, constructed, and has now recently begun splitting atoms, in Georgia. But unfortunately, in part because of the extremely high regulatory burden imposed during construction, the project came in about seven years and $20b over its initial budget – and, along the way, led to the bankruptcy of Westinghouse, a major player in the industry.

So…the US might just take the crown for world’s most onerous nuclear policy & regulatory regime. But at least we’re not Germany, where it’s downright illegal to build new plants, and the government spent the past decade shutting down perfectly good plants that were already operational.

Meanwhile, nations with friendlier public opinion & rational regulatory stances towards nuclear energy have continued to build new plants at a reasonably competitive cost, with more or less the same Gen II light water reactor technology that the US pioneered in the 1960s.

I’ll repeat myself, because this point is so important. Nuclear deployment does not, fundamentally, require new technology. However, new technology might make a difference in addressing the root problem of public acceptance.

There are two primary technology pathways that nuclear fission companies have been pursuing (which aren’t mutually-exclusive). The first path is towards small, modular reactors, or ‘SMR’. The thesis behind SMR is that serial, factory-based production of reactors can make them cheaper & more flexible to deploy – even if those reactors use the same coolant (light water) and other core design parameters of established, large-scale reactors.

Whether this vision for SMRs will work out in practice remains a subject for debate. We know from experience that there are economies of scale in the construction of single, massive power plants…while economies of scale in serial factory production of reactors remain theoretical. One big outstanding question is what volume of orders an SMR factory would need to really get cranking - to make good use of the capital spent on the factory, and to begin progressing down the type of learning curve that tends to apply to manufactured products.

More importantly: Will going small & modular address nuclear’s more foundational public perception woes? I don’t believe that it will - at least, not on it’s own. That’s where another set of nuclear innovation pathways comes into play. The first of these pathways is often labeled “Gen III”, which is distinguished from Gen II by new design features which emphasize “passive” safety - in other words, in the event of a plant-wide outage, these reactors will cool down on their own.

The goal of Gen III nuclear approaches is to dramatically increase safety – and just as importantly, public perception of safety – while minimizing the R&D and regulatory risk inherent in any other major changes to Gen II designs (e.g. fuel, pressure, etc). NuScale’s 50 MW reactor is a standard bearer in this category.

“Gen IV” contains a much wider field of novel reactors pursuing some combination of superior safety profile, fuel cycle, physical footprint, and output temperature - by employing a diverse mix of fuel grades, coolants, operating pressure, and reaction speed. Dozens of startups have entered the market with novel designs.

This proliferation of startups is mostly a positive sign for nuclear, but I suspect to some degree a surfeit of options might also be holding the industry back. In my experience, if you ask fifty nuclear experts which next generation approach is the best one, you might get close to fifty different answers. Yet the prospects for a nuclear renaissance writ large would be much better served by fifty deployments of one new reactor design than by one deployment of fifty new reactor designs apiece. This is especially true, of course, for SMR, as they’re particularly reliant on volume production to achieve lower cost.

Ironically, the US is home to many of the companies developing next-generation nuclear technology, but for reasons discussed above we’re not on track to be the testing ground for that technology. Other regions with less abundant renewable resources have unsurprisingly been the first to arrive at the conclusion that it’s “when”, not “if” for nuclear. Hence, East Asia & Eastern Europe are emerging as the most likely ‘Florences’ of the coming nuclear renaissance. My expectation is that policy preferences in these countries – including domestic industrial preferences – are likely to be more influential than a nuanced review of 50+ reactor designs in determining the next-generation of winners.

When (not if) the US does wake up to the need for accelerated nuclear deployment, hopefully we’ll be able to benefit from new technology & supply chains already scaling up among allied nations.

On the other hand…

“Nuclear” does not necessarily mean nuclear fission. In fact, theoretically, the primary resource gap I described at the beginning of this essay doesn’t need to be filled by “nuclear” at all. It could instead by filled by something “nuclear-esque” which shares nuclear fission’s basic profile: inexhaustible, zero-carbon primary energy generation packed into a power-dense, geography-independent, baseload frame (“…seeking zero-carbon energy consumers for a long-term relationship”).

One such option is nuclear fusion. Fusion’s big advantage over fission is that it’s an inherently safe reaction (i.e. no runaway potential) which yields dramatically lower-level radioactive waste. Hence, theoretically, fusion ought to be able to win over public opinion and be regulated with a much lighter touch than just about any fission solution.

The perennial joke about fusion is that it’s been “twenty years away” for the past fifty years. Now, thanks to a surge in private venture investment in fusion technology companies, there’s a pretty darn good chance that it’s finally, actually within striking distance.

“Within striking distance” means close to demonstrating key scientific milestones – which is far from implying commercial success. There’s a good chance that within the next few years, one or more fusion companies will announce that they've achieved “energy break even”, or some important indicator of it’s potential.4

This would be an incredible scientific achievement. However, fusion must be achievable cost-effectively in order to matter to the energy system or the climate. Most current approaches to fusion require either A) extremely expensive superconducting magnets shaped with near-perfect precision into giant, hollow donuts; or B) dozens of extremely expensive, ultra-powerful lasers that don’t quite exist yet; or C) both. (EIP’s portfolio company, Zap Energy, requires neither, which is one of many reasons we’re especially excited about Zap’s commercial potential.)

So, I’m excited about fusion…but humanity can’t bet the farm on it. What else is out there that’s “nuclear-esque”? The most obvious answer is geothermal energy. It’s zero-carbon, accessible anywhere on the planet, and effectively inexhaustible if one can drill down deep enough into the earth. …And there’s the rub.

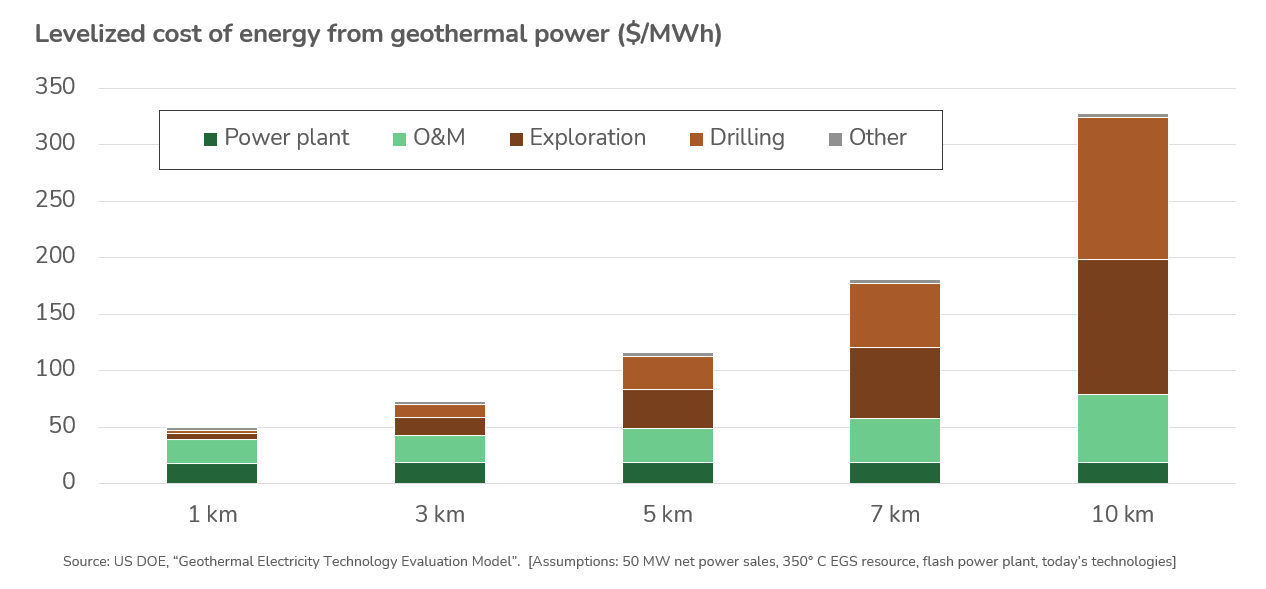

Accessing high temperature geothermal heat is challenging for many reasons. Geothermal development has a similar exploration risk profile as oil & gas, but with a much smaller reward for successful discoveries. (Liquid fuel is just way more valuable than heat.) Most importantly, to make geothermal energy truly “nuclear-esque” would require super deep drilling.

Heat sufficient to fuel power generation and most industrial processes is available about 10 miles underground nearly everywhere on earth. Even the ability to reach 5 miles underground, affordably, would unlock a wealth of new geothermal resources. But today the amortized cost of drilling to these depths alone is about five times the levelized cost of energy from wind or solar power.

Hence, a technology game-changer in deep drilling & geothermal power production would be practically equivalent to fusion. We haven’t yet made an investment in this space at EIP, but I’m nonetheless crossing my fingers for success.

Until then, I’m forced to wait (impatiently) for the world to get really serious about nuclear - and in particular, for the stirrings of a nascent, global nuclear renaissance to take hold here in America.

Lastly…for all you nuke-nerds: Thanks to my colleague Johnny Daugherty at EIP, here’s a nice graphic summarizing major Gen IV reactor concepts:

Enjoy this post? Please check out the rest of the Ten Biggest Questions in Energy & Climate Tech

I say “ideally” because firm capacity is only necessary if we aren’t able to balance intermittent renewable power generation and energy demand using a modest amount of cost-effective grid storage…and I’m fairly convinced that we will be able to do so.

For the uninitiated, “capacity factor” is a ratio of the energy that a power plant actually generates in a year relative to the maximum output it would have generated if it were running at full tilt, all the time. At best, wind farms hit about 50%.

In Fukushima, many people were tragically lost to the destruction wrought by the tsunami, and nuclear meltdowns led to a massive loss of property in the evacuation zone…but nobody was killed by the nuclear disaster.

A recent announcement to this effect by the National Ignition Facility in the US did not actually come close to qualifying as “break even” in terms of full system energy balance.

Is there a hidden carbon issue with Nuclear due to the embodied carbon from all the cement used to make a reactor? Have you seen any reliable calculations on this question?