It's time to build! (light water reactors)

Charts of the week

Today’s chart comes from the US Department of Energy’s “Pathways to Commercial Liftoff: Advanced Nuclear” report.

In case you haven’t been paying attention: Southern Company recently completed the first two new large nuclear reactors in the country in about 30 years at Plant Vogtle.1 These were both Westinghouse AP-1000 Pressurized Water Reactors, which are classified by the nuclear industry as “Generation III+” units. The ‘plus’ stands for substantial improvements in passive safety over the prior generation of reactors, which all use “light water” (basically just plain, old water) as a coolant and neutron moderator. The ‘1000’ denotes that this is a large-scale reactor. There’s nothing small or modular about it — these things produce over 1,000 megawatts of power.

So naturally, one strategy for reducing the cost of nuclear energy in the United States — and probably elsewhere — would be to continue building more Gen III+ light water reactors. Specifically, there’s a strong argument for simply building more Westinghouse AP-1000s. It doesn’t take a degree in nuclear physics to comprehend why building more of the same kind of facility, over and over, should result in lower costs and faster construction timelines. This is Econ 101 material: Supply chains benefit from scale. People learn by doing.

This is basically the conclusion of the DOE’s Commercial Liftoff report. The authors estimate that the next set of AP-1000s would take about 45% less time & money to build. Factoring in incentives that are currently available from the Inflation Reduction Act, and debt financing from the DOE Loan Programs Office, the levelized cost of energy from the next AP-1000 could be as low as $60 per MWh.

Notes:

$60/MWh would be an extremely attractive price from a firm, power-dense source of zero-carbon energy. There’s really nothing else quite like it.

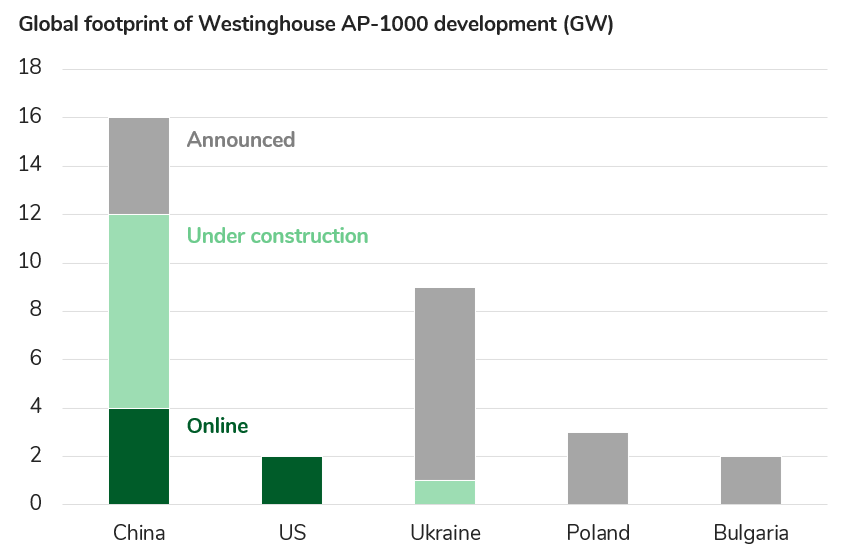

Yet there is not a single new AP-1000 announced or under development in the US. Hmm…

Meanwhile, small modular reactors (or SMRs) are continuing to attract attention here in the US, and globally. In particular, it appears as though GE-Hitachi’s BWRX-300 reactor design may have reached a commercial inflection point. (More on this below.)

This attraction to SMRs is a bit of a puzzle, because nearly all of the nuclear experts I know believe that the first few projects for any given SMR technology will almost surely be more expensive than another set of AP-1000 projects (provided those AP-1000 projects are reasonably well executed). And therein lies the rub for large reactors, and the biggest advantage for SMRs. Large reactor projects are generally perceived as facing a much higher risk of cost overruns… and those theoretical cost overruns are, by definition, much bigger sums. This perception, combined with SMRS’ greater suitability for expansions of existing nuclear plants or utilization of retiring coal plant sites, has given SMRs a powerful wedge into the market.

This DOE report postulates that any new SMR design will require roughly 5-10 committed orders to achieve commercial “liftoff” — meaning a reasonably robust supply chain & standalone economic competitiveness. Of all the SMR vendors, GE-Hitachi appears most well positioned to pass this critical commercial threshold in North America, with two near-term projects in the works, three currently planned for the mid-2030s, and the potential for two more procured through competitive processes.2

International nuclear development, on the other hand, still skews heavily towards larger reactors like the AP-1000. We’ve tallied up announcements totaling 26 new AP-1000 units outside of the US, which ought to give Westinghouse and its critical suppliers an even better chance to pull ahead when it comes to deployment cost.

On that note, nuclear technology exports continue to be an important vector for geopolitical competition. This is one of the few areas in which Russia has remained a leading tech player — with a nuclear industry bolstered by generous state financing support, and a loose regulatory environment when it comes to non-proliferation. However, South Korea and France also have developed successful export programs, and the Chinese government’s “Belt and Road” initiative calls for exporting at least 30 domestically designed reactors by 2030. It will be nearly impossible for the US to remain competitive as a reactor technology exporter without a meaningful level of domestic deployment… This is yet another reason why it’s time to build more light water reactors!

What about “Gen IV” reactor companies — such as Kairos, X-Energy, Radiant, and Terrapower — which make use of coolants beyond light water? A number of these companies have also made good progress in 2024. Kairos won a 500 MW deal with Google, plus NRC approval for a demonstration reactor. X-Energy announced a 960 MW deal with Amazon and Energy Northwest. Radiant advanced to “Detailed Engineering and Experiment Planning” at the Idaho National Lab. And Terrapower broke ground on its Natrium demonstration project in Wyoming.

Gen IV technology can theoretically serve a number of applications which are simply not suitable for light water reactors — such as industrial demand for high temperature process heat, as well as combined heat & power. They’re also better suited for even smaller “microreactor” form factors, and for utilizing spent fuel from light water reactor cycles.

So, there are plenty of good reasons to be encouraged by progress on Gen IV technology. However, I still believe that Gen IV is unlikely to be competitive with light water reactor technology — at least, as a globally relevant power generation resource — for several decades to come. Hence, in my view, we should view Gen IV technology as additive to our existing slate of light water reactors, not as a substitute for Gen III+ deployment in the 2020s and 2030s.

Remember, what matters to the climate is the total stock of carbon in the atmosphere. It’s important to get moving on the next tranche of reactors we can build with confidence as soon as possible.

Want more nuclear material?

First, please subscribe… (it’s free!)

Also, check out the second in my ten part series on the biggest questions in energy & climate tech, “When Will we Get Serious About Nuclear?”

This doesn’t include Watts Bar Unit 2, which was completed in 2015, but actually began construction way back in 1973!

AEP announced plans to begin an Early Site Permit application for an SMR in Virginia (Nov 2024)

Dominion launched an RFP to add an SMR at an existing nuclear plant in Virginia (July 2024)

TVA committed an additional $150m in funding for their Clinch River project, which is expected to be the first SMR in the US and will use GE-Hitachi’s SMR (Aug 2024)

In Canada, Ontario Power Generation announced that they plan to begin construction in 2025 for their Darlington project, which will be the first SMR in North America and will also use GE-Hitachi’s SMR. They plan to complete construction by 2028 and deploy three additional units between 2034-36 (Sept 2024).